The ongoing noise around fintechs affects bank CIOs’ ability to engage with them.

Two years ago, Jamie Dimon, chairman and CEO of JPMorgan Chase, wrote in a letter to shareholders, “Silicon Valley is coming.”

Since then, there has been a dramatic rise in interest and investment in the fintech market. In the first half of 2016 alone, investment in fintech companies exceeded $15 billion. A Google search for “fintech” in February 2017 returned more than 19,300,000 results.

Speaking at the Gartner IT Infrastructure, Operations & Data Center Summit in Sydney this week, Alistair Newton, research vice president at Gartner, said the ongoing noise around fintech creates confusion for CIOs and other bank executives.

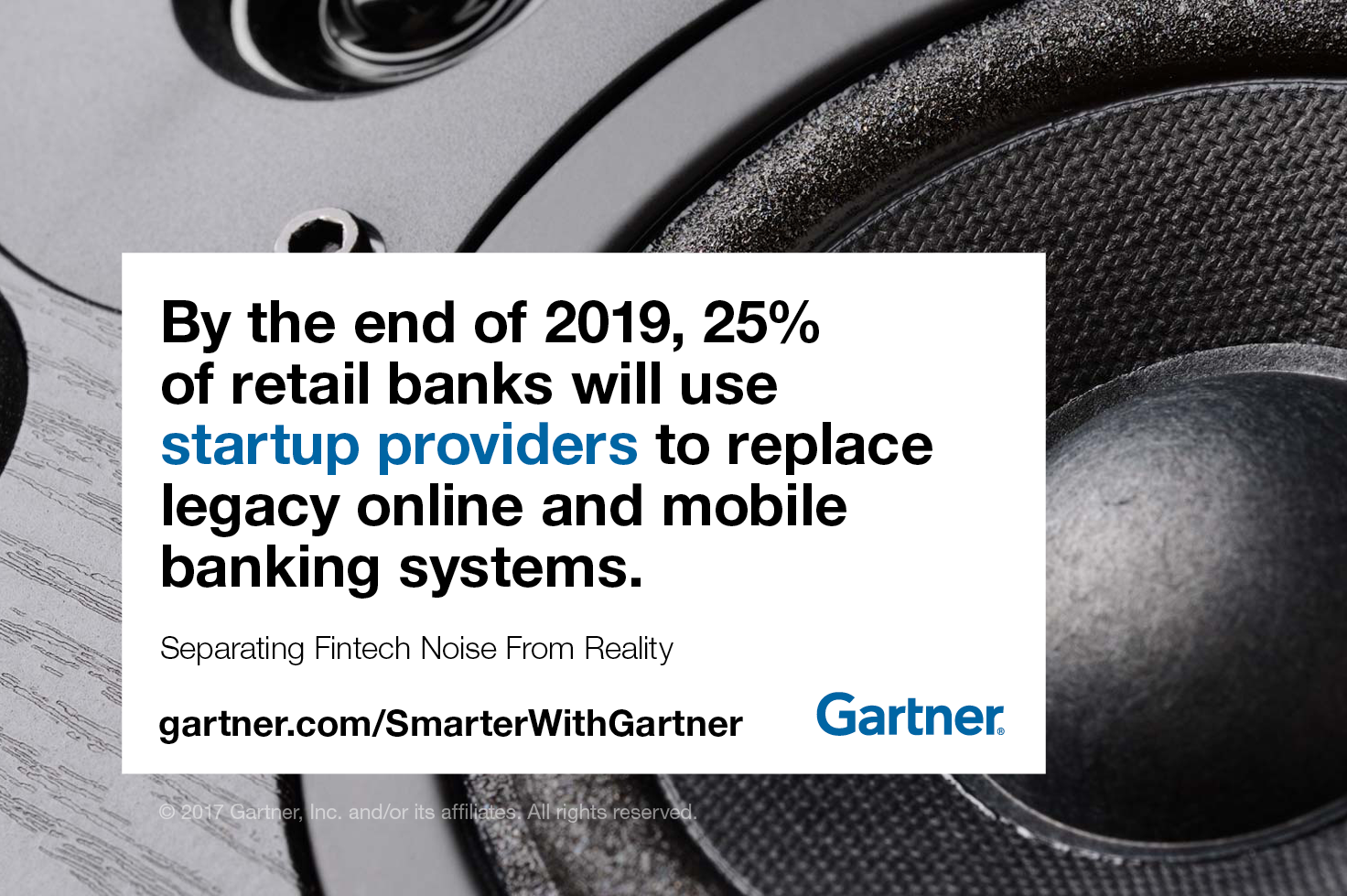

By the end of 2019, 25% of retail banks will use startup providers to replace legacy online and mobile banking systems.

The noise comes from overuse use of the term “fintech”, used to describe firms big and small, new and old, pure-play startups and entrants from other industries. Venture capital funding, accelerator and lab announcements add to the noise and are not necessarily related to the adoption or success of the technology.

“The hype presents a significant obstacle to bank CIOs’ ability to make well-informed decisions about how to engage with fintechs,” Newton says. “It also fuels demands from the business for CIOs to answer questions as to why their banks are not using fintechs, competing more aggressively with fintechs or acquiring fintechs.”

To help CIOs determine the real value of fintechs to their organizations, Gartner provides this definition:

Fintechs are startup technology providers that deliver emerging digital technologies that approach financial services in innovative ways or can fundamentally change the way bank products and services are created and distributed, and generate revenue. The term may also refer to the technologies these providers offer.

Threats or Opportunities?

Most financial services firms look at fintech companies as friends or foes, says Newton, but a premature use of that dichotomy can lead to bad strategic decisions.

In reality, the transformational technologies that banks need are increasingly being developed by fintechs, which presents both threats and opportunities for banks.

Fintechs threaten the foundational services that banks offer customers and revenue. They often focus on simple, easy-to-use apps that charge consumers lower fees — or no fees at all — for transactions.

However, fintechs also offer bank CIOs an opportunity to deliver the emerging digital technologies their institutions need and their customers demand, quickly and cost-effectively.

Gartner predicts that by the end of 2019, 25% of retail banks will use startup providers to replace legacy online and mobile banking systems.

Cost optimization or digital transformation?

Fintech startups generally offer either opportunities to help with transformational digital strategies or opportunities for IT cost optimization. Rarely will a fintech be able to address both. Bank CIOs can use fintechs to:

1. Drive IT cost optimization

Some fintechs offer CIOs the opportunity to improve customer experience or solve a specific financial services problem. These issues often result in customers turning to branches or contact centers to perform tasks, abandoning account opening applications or simply deleting mobile apps — all of which contribute to higher costs.

To use fintechs that support IT cost optimization, CIOs should purchase access and use APIs to deliver these fintech capabilities through the bank’s mobile app, website or even a third-party app or site. Alternatively, if the bank has sufficient internal IT skills, the CIO might consider building a similar capability in-house.

2. Support digital transformation

Fintechs that facilitate digital business have the potential to fundamentally change the way the bank does business and to generate revenue.

Bank CIOs should invest in or partner with these types of fintechs. For example, to gain access to blockchain solutions, Commonwealth Bank of Australia has partnered with Ripple, while BBVA Compass has partnered with Wave.

“CIOs evaluating fintechs need to focus on the additional benefits that fintechs provide, including increased agility, improved customer experience, new services or brand differentiation,” says Newton. “Clarify the debate by clearly articulating the threats and opportunities to the bank.”

Get Smarter

Client Research

Gartner clients can learn more about working with fintechs in the report: How Bank CIOs Can Make Fintechs Work for Them.

I&O Hub

Visit Gartner’s Infrastructure and Operations hub for complimentary research and webinars.

Gartner Global Infrastructure & Operations Events 2017

Data center issues and IT operations will be further discussed at the Gartner Global Infrastructure & Operations Events 2017 in Mexico City, Mexico; Mumbai, India; Sydney, Australia; London, UK; and Las Vegas, NV. Follow news and updates from these events on Twitter using #GartnerDC.