Many blockchain concepts are immature, poorly understood and unproven in mission-critical, scaled business operations.

Your CEO reads in a newspaper or magazine that “blockchain is the ‘next big thing’.” At the office, the CEO summons the CIO and asks: “Is our company doing anything about blockchain? Everyone says it’s the next big thing!”

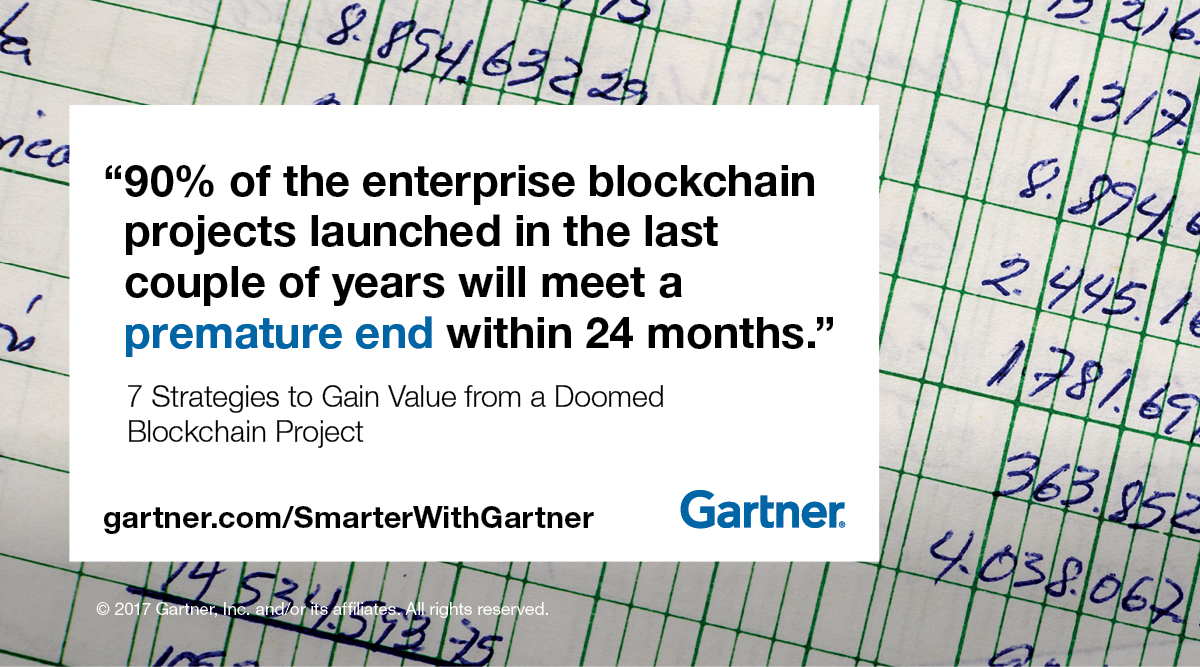

Despite the hype, blockchain technology remains the subject of much confusion. This confusion has led many enterprises to launch misconceived blockchain projects that are likely to fail. In fact, Gartner predicts that 90% of the enterprise blockchain projects launched in 2016 and the first half of 2017 will meet a premature end within 24 months.

“There are multiple causes for disappointing project outcomes, including rapid rate of technology evolution,” said Ray Valdes, vice president and Gartner Fellow. “However, a primary cause of failure is a fundamental lack of understanding around the basic concept of blockchain technology, which results in a misalignment of its capabilities with the business problem that the enterprise is seeking to solve. Often this means that enterprise projects using — or claiming to use — blockchain technology don’t actually need it to achieve their goal.”

Read More: A CIO’s Guide to Blockchain

The good news is that despite shaky underpinnings, many enterprise blockchain projects do still have potential value. Even when such projects are already underway, it’s often possible to derive value from them by taking time to really understand the technology and making some strategic corrections.

Here are seven strategies for salvaging value from your “pointless” blockchain project:

- Narrow the scope to a concrete, achievable business goal

All too often, ambitious projects that have been positioned as strategic, transformative and innovative come with a high probability of failure. This can be averted in the early stages by narrowing the scope of a project to something that the current generation of blockchain technology can handle. This basically involves reducing the project down to a sequential, flat-file record of significant events or transactions with no sophisticated data model, no smart contracts and a low transaction volume. - Expand the non-blockchain parts of the project

The non-blockchain elements of the project will have a higher probability of delivering value within the constraints of time and budget. Imagine you have embarked on an ambitious application rationalization and modernization project. If it was primarily based on a blockchain, the technical risk would be high due to the technology’s immaturity. Instead you could build on the project’s conventional technology, such as a distributed DBMS platform, which might enable you to achieve similar benefits with less risk. - Prepare to migrate

Considering the rapid evolution of blockchain technology, it’s likely that whatever technology you select today will be the “wrong” one in the long term. It makes sense, then, to plan to migrate to a next-generation platform within 18 to 24 months. In this way, the data captured in the initial deployment effectively becomes the foundation that will be built upon in future deployments. - Expand the community

Another issue with ambitious projects is that they tend to require highly skilled staff to run them. However, making some or all of the solution open source can open up the labor pool, reduce development costs, make it easier to hire experienced staff and increase brand value. Likewise, in building a solution on a blockchain technology platform, favor the open source platform because at this moment, those platforms have a larger ecosystem of developer talent than closed-source proprietary platforms. - Declare an early victory and cut your losses

If you’ve divided your blockchain project into well-defined phases, don’t be afraid to celebrate an early victory after the first phase. Learn whatever you can from this phase, and use that knowledge as the basis for planning further phases. At this stage you can fine-tune the next phase, which could include making a platform change, an architectural shift, a scope change or even an early termination. - Capture integration points

Blockchain applications may not exist exclusively in the domain of digital currency platforms, and must integrate with other systems that provide access to real-world data and events, such as smart contracts. If the integration points have appropriate API design and layers of abstraction, they can live on beyond the initial blockchain application. APIs can enable different kinds of foundational technology, not just blockchain technology, to be incorporated as part of the overall solution. - Cultivate and preserve new skills

Developing blockchain applications requires new kinds of skills that won’t always be present in most enterprises’ IT organizations. Even if the original project doesn’t go the distance, experience with these new skills will prove valuable for subsequent projects in the era of the “programmable economy” (or what others term the “Internet of money”).

Get Smarter

Client Research

Gartner clients can read more in “How to Make the Most of a ‘Pointless’ Blockchain Project.” This research is part of the Gartner Trend Insight Report, “Practical Blockchain,” a collection of research around the practical realities facing CIOs, business leaders, developers and other potential adopters of blockchain technology.

CIO Conferences 2017

Gartner analysts, and industry leaders will discuss key issues facing the CIO during Gartner’s CIO conferences taking place May 8-9 in Magaliesburg, South Africa, May 18-19 in Munich, June 6-8 in Toronto and August 29 – 31 in Cancun. You can follow news and updates from the event on Twitter using #GartnerCIO.